The Economic Script Has Changed

A New Reality

In most of my blog posts, I have written about societal scripts: gender scripts, self-worth scripts, ambition scripts. The invisible narratives that shape how we move through the world without ever consciously agreeing to them.

Today, I want to focus on the economic script. Because something has shifted. Structurally.

We are living through a period of economic disorientation. Most people are working hard, doing what they were told was sensible, ticking every responsible box; and yet stability feels further away, not closer. When structural economic shifts make life materially harder but cognitively opaque, frustration becomes inevitable. And that frustration turns moral very quickly.

The Old Script: Work, Save, Wait

For decades, the moral story was clear:

Work hard

Save consistently

Delay gratification

Avoid risk

The system will reward you.

Saving was not just financial advice, it was a virtue. It symbolised discipline, responsibility, maturity and foresight. If you deferred pleasure and accumulated cash, stability would follow. And for a long time, that story largely mapped on to reality.

Cash was king.

Money in the bank held its value. Property was accessible to ordinary earners. Wages and living costs were not perfectly aligned, but they moved in a way that made planning possible.

But that script no longer reflects the environment we are operating in.

The Quiet Structural Shift

What makes this moment so destabilising is not just rising costs or political turbulence. It is that the reward structure of the system has changed.

We are now living in an era defined by:

Persistent inflation

Asset price inflation (property, equities, land)

Currency dilution

Volatility

Concentration of ownership

In this environment, cash does not behave the way it used to.

To make this concrete: if inflation averages 4–5% and your savings account earns 2%, your money is quietly losing purchasing power each year. Nothing dramatic. Nothing visible. Just erosion.

The “safe” option no longer guarantees stability. In many cases, it guarantees stagnation.

This is why so many people feel as though they are working harder yet treading water.

If that is you, I want to say something clearly: the problem is probably not you. It is that the economy you are operating within has changed.

Of course, not everyone has equal starting conditions, but understanding the system still matters, regardless of where you begin.

Why This Debate Gets So Moral

When people argue about the economy today, they are rarely just arguing about policy. They are arguing about fairness. About effort. About whether discipline still pays off. Because at the heart of the old economic script is a moral promise: If you behave responsibly, you will be secure. When that promise breaks, it feels like betrayal. So we look for someone to blame: governments, corporations, older generations, younger generations, the wealthy, the system itself. But much of the anger is actually confusion.

We are applying a moral framework built for a previous economic era to a structurally different one.

Stability Now Comes From Position

Here is the uncomfortable truth.

Stability today comes far less from effort alone and far more from position.

Your relationship to assets

Your exposure to inflation

Your proximity to ownership

Your ability to withstand volatility

This does not mean the system is evil. It does not mean saving is pointless. It does not mean effort no longer matters. But it does mean that much of the traditional advice is incomplete.

If you are simply saving cash while asset prices rise faster than your savings grow, you are not irresponsible. You are following a script that no longer maps on to reality. And that mismatch creates anxiety, shame and political rage.

What Thriving Looks Like In This New Era

If stability now comes from position rather than effort alone, then the question becomes: “how do you position yourself?”

In this era, economic literacy is no longer optional.

Not in a frantic way. Not in a “get rich quick” way. But in a strategic, grounded, long-term way. Let’s begin with the most emotionally loaded topic: homeownership.

Everyone is still fixated on the old script that says stability equals owning your primary residence. And to be clear, I am a homeowner. I see the benefits. There is psychological security in it. There is protection in it. There is long-term leverage in it. But if I’m honest, my path to homeownership was more about being financially prepared when the opportunity presented itself than following a deliberate blueprint.

The issue is not homeownership. The issue is treating it as the only route to stability.

In this new economic era, ownership matters more than geography. If you cannot afford to buy in your city, that does not mean you are locked out of ownership altogether. It may mean buying in a different, more affordable location. It may mean purchasing something smaller. It may mean renting where you live and owning elsewhere.

For example, someone priced out of London may be able to purchase in a northern city with stronger rental yields. They may not live there but, they are still participating in asset appreciation rather than standing entirely outside of it.

The new script requires strategic problem solving.

You may not be able to play the game the way your parents did, but that does not mean there is no game to play.

Investing Is The New King, But Boringly

In the old script, cash was king. In the new one, intelligent investing quietly is.

Not speculative trading. Not chasing trends. Not reacting to every headline. Boring, long-term investing. The kind that compounds slowly. The kind that protects against inflation. The kind that feels underwhelming in the short term.

If someone invests consistently over thirty years, the power of compounding does more heavy lifting than any dramatic market timing ever could. It is not exciting. It is not glamorous. But it works.

Avoiding get-rich-quick schemes. Accepting that wealth, unless inherited, usually accumulates slowly. Wealth rarely comes from adrenaline. It comes from time.

Cash is still important. Liquidity matters. Emergency funds matter. Flexibility matters. But holding excessive cash while inflation erodes its value is not safety, it is slow leakage.

The Generational Narrative We Need To Let Go Of

It may be true that previous generations had structural advantages: cheaper housing, stronger wage-to-cost ratios, defined benefit pensions.

But this generation has different tools. Defined contribution pensions allow for early compounding over decades. Investment platforms are accessible. Financial information is widely available. Barriers to entry into markets are lower than they have ever been. Time is an extraordinary asset; particularly for younger people who start early.

Yet many are psychologically paralysed by comparison. We were raised with a script that said life should be easier than our parents’. That progress is linear. That each generation moves materially upwards. When that does not happen, or does not happen in the same way, it creates deep psychological stress. It feels like regression. Like failure. Like something has been taken. But comparison to a past economic era is not a strategy. Holding on to the expectation that life must look easier than it did for our parents can become a source of chronic resentment.

Letting go of that expectation is not surrender, it is adaptation.

The question is not whether this era is harder. The question is: what does this era reward?

Asset-Driven Thinking

In this economy, income sustains you. Assets stabilise you.

That might mean:

Pension contributions that compound for thirty+ years

Broad, diversified investments designed to outpace inflation

Property in strategic locations

Ownership stakes in businesses

Skillsets that increase bargaining power and income resilience

This is not about luxury. It is about insulation.

Wealth inequality will likely continue widening, not simply because of greed or political failure, but because asset ownership compounds and cash does not.

If people focus only on fairness debates and political outrage while ignoring positioning, the gap widens further.

Governments operate under competing pressures: pleasing older voters, inspiring younger ones, attracting corporate investment, maintaining economic stability. Structural change is slow because it must balance multiple interests.

Your life, however, is moving in real time.

You can absolutely hold moral convictions. You can advocate for fairness. You can care deeply about the kind of society you want to see. But at the same time, you have a responsibility to secure stability for yourself and your family within the system as it currently exists. These positions are not contradictory. You can fight for how things ought to be while making decisions based on how things actually are.

Peel Back The Morality

If you want clarity right now, the most important question is not:

“Am I working hard enough?”

It is:

“What is this system actually rewarding?”

When you remove moral judgement from the analysis, you can see more clearly. That clarity allows for strategic decisions rather than reactive ones. The script has changed; we are not simply living through a downturn or a temporary crisis, we are living through a shift in the underlying script.

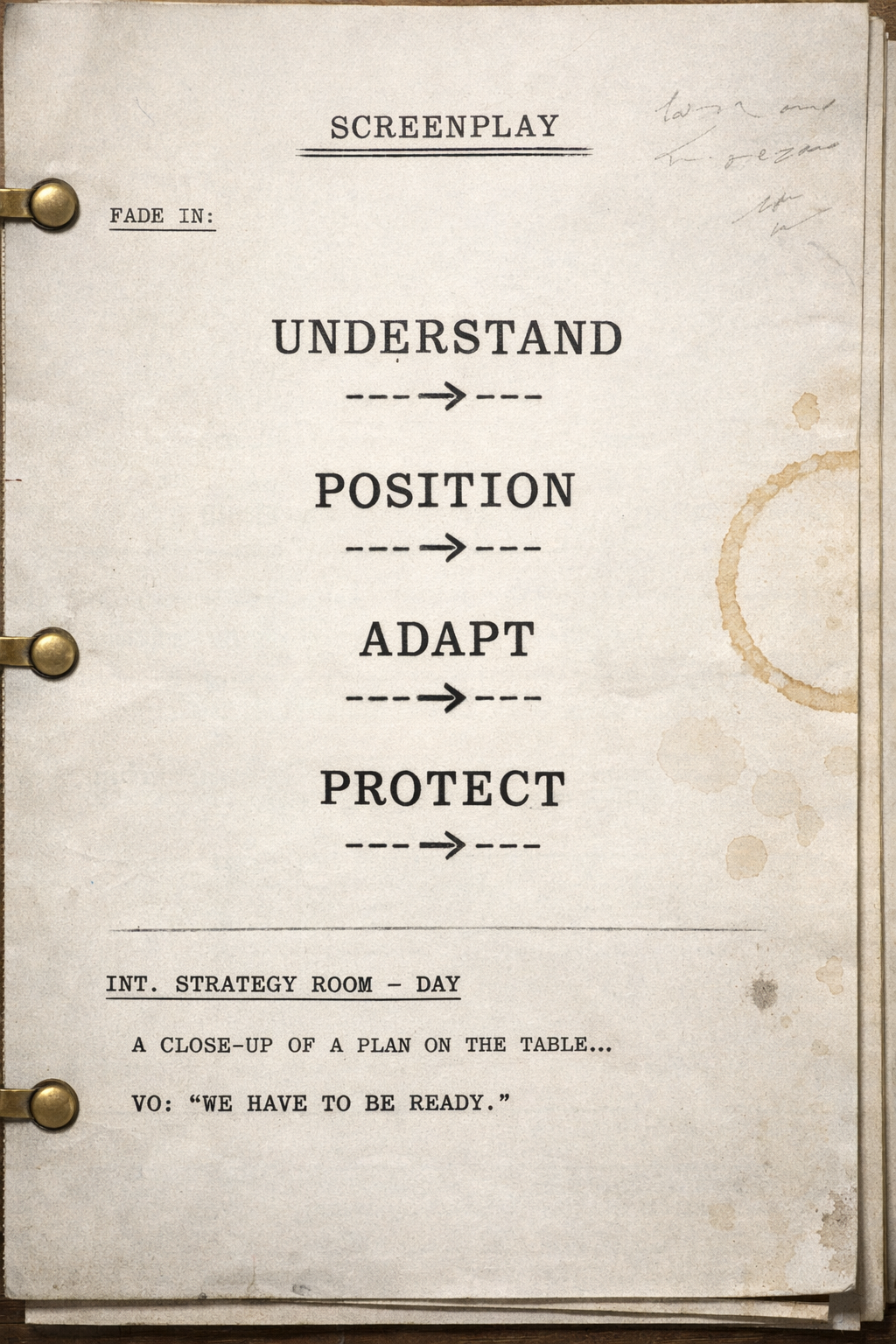

The old story said:

Work → Save → Wait → Stability

The new environment says:

Understand → Position → Adapt → Protect

It may feel uncomfortable. It may feel unfair. It may feel as though the rules changed mid-game. But ignoring the shift does not protect you from it. Understanding it does.

The system has changed. The question is whether you will.